Chart of the Day: AI is Eating Markets | Paul Kedrosky

body

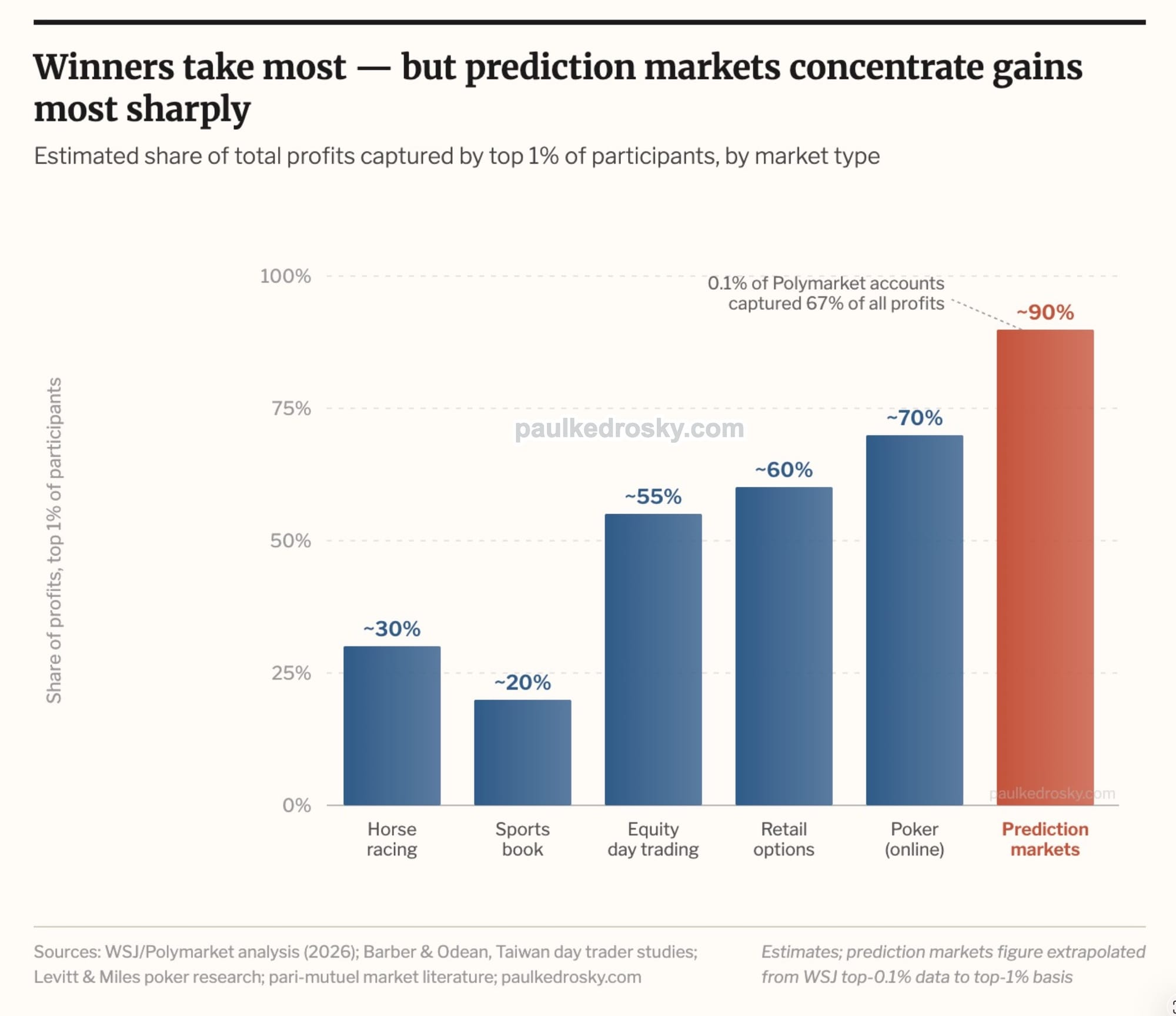

The return skew in prediction markets' returns is startling. It is partly a function of their nature, but also of vibe-coding script kiddies attacking every market anomaly as quickly as it arises. Check a recent WSJ article for examples.

The same dynamic is now spreading across retail-dominated markets. A driver is how AI lowers the cost of systematic exploitation and exploration to near zero. What used to require infrastructure, data pipelines, and bearded quants is now accessible via off-the-shelf models, APIs, and loosely stitched “agent” workflows doing... stuff that even their users don't fully understand.

The result isn’t democratization of returns. It is wider participation, of a sort, alongside the rapid re-concentration of profits. A small subset of users—those willing to iterate fastest, monitor continuously, and deploy capital programmatically—capture gains, with everyone else just liquidity.

They scrape sentiment, parse new information, and reprice positions in seconds, compressing the half-life of mispricings. That doesn’t eliminate inefficiency, but changes who harvests it. The edge shifts from insight to speed, coverage, and execution discipline—areas where even modest automation compounds quickly, and edges disappear overnight.

Prediction markets are simply the cleanest expression of this trend because they combine thin liquidity, discrete outcomes, and high retail participation. But the same pattern is visible in options flow, single-stock volatility events, and even online poker, which AI increasingly dominates.

As AI tools continue to scale, expect this to get worse: a small cohort running semi-automated strategies extracting semi-consistent edge, and a much larger base supplying them returns. Under the pressure of AI prevalance, markets don't flatten, the return gradient steepens to a cliff.