I make good money. Why do I still feel like this? | Hanna Horvath

body

The middle class was a policy project. Every piece of it has been unbundled and repriced — and now two very different groups are living two very different nightmares.

I have horrendous work-life balance. I know this about myself. I built a career in financial journalism, started this newsletter, took on financial planning clients, and somewhere along the way adopted a pace that I would never, ever, tell someone to adopt.

The main reason why I am the way I am is rooted very much in my money anxiety.

By most objective measures, I’m doing quite well, financially. I can more or less make decisions without thinking too much about the cost of things, and I feel statistically “on track” (whatever that actually means).

But there’s this hum underneath everything. This feeling that no matter how much I accumulate, I’m never going to feel financially “okay” — which is as much a state of mind as it is a number. In other words, I’m not great at taking my own advice.

I know I’m not alone in this, because you tell me. Every week, in my comments and my DMs, some version of the same confession: I make good money. I have $xyz in my bank account. Why do I still feel like this? Why do I feel so behind? Why does this all feel like a treadmill I can’t get off of?

The feeling you have probably isn’t one of deprivation. It’s dissonance.

I’ve been writing about the K-shaped economy for a while now — this idea that the post-pandemic recovery didn’t lift everyone equally but instead split into two trajectories. The top of the K (asset owners, high earners, people who bought homes before 2020) mostly recovered and then some. The bottom of the K (wage workers, renters, people without generational wealth) fell further behind.

One consequence of that divergence is the hollowing out of what we used to call “the middle.” Under a capitalistic model, companies tend to innovate where the money is — more sales at higher margins means more value for shareholders. So when wealth concentrates at the top, that’s where the products and services follow.

I wrote about this in “The tierfication of everything” — how companies are increasingly designing for two customers: premium and budget. And it’s mostly premium. You see this in the airline industry, healthcare, groceries, housing. It’s known as the “missing middle”.

So what happens to the people who used to live in that middle?

Two things. Some people are experiencing real, material deprivation — the basics are genuinely slipping away. But a lot of people — and I think this includes much of this newsletter’s audience — have money. They just aren’t affording the life they thought they would have by now.

And the distance between those two experiences — and the way both groups misdirect their frustration — reshapes how we think and behave with money. It fuels financial nihilism, doom spending, low trust, and a creeping sense that the whole project of “working your way up” might be broken.

The middle class was a policy project

The American middle class as we know it didn’t emerge from the free market. It was constructed — deliberately, through policy, in response to specific political and economic conditions.

After World War II, the government faced a crisis: 16 million veterans were about to flood the labor market, and policymakers were terrified of a repeat of the Great Depression. So they turned to policy. The GI Bill offered zero-down-payment home loans and free college tuition. FHA and VA loan programs fueled suburban construction. The Wagner Act protected unions, so a factory worker could bargain for better wages. Employer pensions meant you had a somewhat guaranteed retirement. Public universities were heavily discounted or free. The top marginal tax rate was around 90%, which funded the schools, roads, and programs that held it all together.[1]

America got a policy-backed bundle of stability that, for millions of families, functioned as middle-class life. And then, piece by piece, it was disassembled.

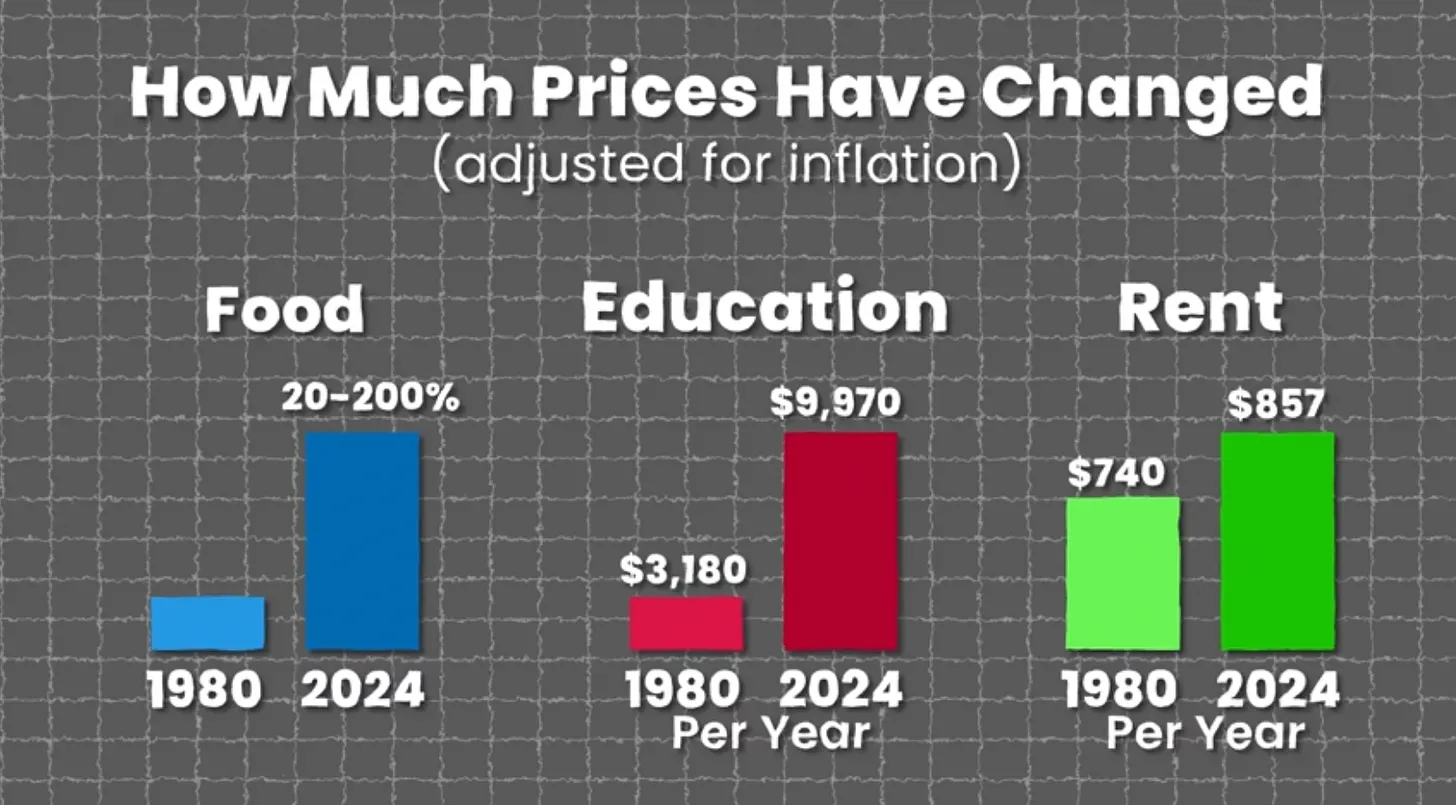

Following came an era of deregulation, the decline of organized labor, the financialization of everything from housing to healthcare, tax policy that increasingly favored capital over wages, and a bipartisan consensus that “the market” would deliver what policy used to guarantee. Pensions became 401(k)s — shifting risk onto individuals. Union membership cratered. Public university tuition exploded. Healthcare became something that could bankrupt you. Home prices are up 60% since 2019 alone. Childcare in 45 states now costs more than the mortgage.

Today, you can earn what used to be a solidly middle-class income and find that it purchases a fundamentally different life than it did a generation ago. Same paycheck, different purchasing power — in part because every component of the safety net “bundle” was repriced individually, and the prices went up.

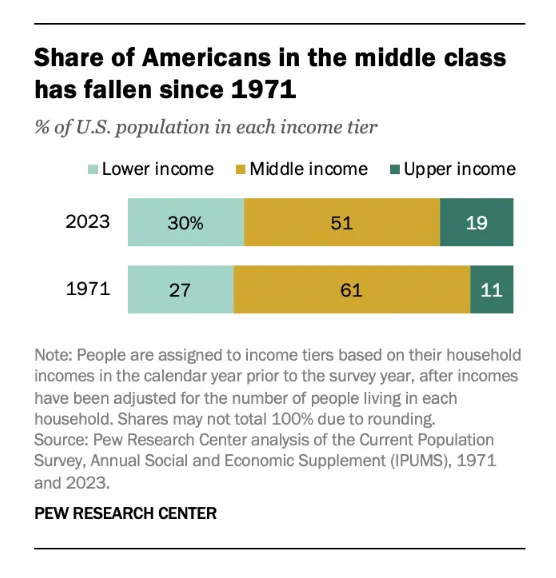

And yet roughly 70% of Americans still identify as middle class, even though only about half objectively qualify. That gap — between who you think you are and where you actually sit is doing a lot of work. “Middle class” stopped being an economic description a long time ago. It became an identity — a story about what kind of life you deserve, what kind of future your kids should expect.

Aspiration drives how we see reality. We’ve always compared ourselves to the people around us — keeping up with the Joneses is as old as suburban cul-de-sacs. But digital culture has supercharged this. Social media collapsed the visual distance between a household earning $85K and one earning $500K.

People also anchor onto milestones, stuff — the house, the car, the school district, the vacation. And because we have a culture built on individualism and meritocracy, when we can’t afford the stuff, or we miss the milestone, we’re more likely to blame ourselves than to critique the system. The ethos of personal responsibility runs so deep that structural failure gets internalized as personal failure.

“Middle class” has become a psychological container that absorbs all of this anxiety — the gap between self-concept and lived experience, between what you were trained to expect and what the economy actually delivers. The term “middle class” holds a feeling. And right now, the feeling is dissonance. “I have what I was told would be enough, and it isn’t, and I don’t know who to be angry at.”

What happens when the middle disappears?

So what’s actually happening to the people inside — and on either side of — what used to be the middle? We get two structurally different versions of the same squeeze.

Material precarity: when the basics slip

If you earn roughly $50K to $100K, have no generational wealth, maybe some college — you’re experiencing what I’d call material precarity.

Material precarity describes people for whom the basics — not the aspirational stuff, the basics — are genuinely falling out of reach. As I said before, the middle class can’t truly be defined as an income number — someone earning $80K in rural Ohio and someone earning $80K in Brooklyn are likely living in different economies.

Instead, it’s about the experience: You’re watching the things that middle-class life used to include by default — stable housing, healthcare that doesn’t bankrupt you, childcare that doesn’t consume an entire salary, a retirement you can actually plan for — slip out of reach. And you know it. You can feel it at the grocery store, at the pharmacy, in the insurance deductible that’s quietly crept up to $8,000.

A Brookings study found that in every single metro area it studied, at least 20% of middle-class earners cannot afford to live there. One-third of middle-class families can’t cover basic necessities. They’re more likely to skip meals, preventative care, more likely to take on debt and fall for predatory financial products. A Century Foundation survey put it this way: “Households with lower incomes are more exposed to corporate practices that leverage their hardship to extract profit.”

That extraction language matters. This group isn’t just dealing with “prices going up.” They’re dealing with an entire consumer economy that’s been redesigned around making the base tier uncomfortable enough to push you toward a premium tier you can’t afford. The degraded version of healthcare, education, air travel, groceries — that’s many peoples’ only option. They’re watching the quality decline while paying more for it.

The psychological effect, from talking to people and scrolling through social media, is a kind of exhaustion. A slow erosion of the ability to plan, to imagine a future, to feel like effort connects to outcomes. This is where trends like doom spending comes from — the logic that if the big goals (a house, retirement, stability) feel permanently out of reach, you might as well buy the small thing that makes today bearable.

Positional precarity: when you have money and it’s still not enough

The HENRY — high earner, not rich yet, gets a bad rap. Though this group makes good money on paper, typically well over six figures, they find themselves in a state of disenfranchisement.

I believe much of this is because their expectations for the kind of life six figures would bring is no longer possible. A household earning $200,000 in 2005 could likely absorb a mortgage, two kids in decent public schools, a yearly vacation, and retirement contributions. That same household in 2026, adjusted for inflation, may find itself running calculations that don’t resolve — the house costs twice what it should relative to income, childcare eating a second salary, and the “good” school district has become its own arms race of tutoring, travel sports, and enrichment programs that didn’t exist twenty years ago.

This explains the quarterly viral Reddit posts about a couple making $800K in NYC who feel like they’re middle class. (I wrote about this last year).

These are overwhelmingly people who come from middle-class or upper-middle-class backgrounds. They have expectations of what their life is supposed to look like — because they watched their parents live it. The upper-middle class has always been aspirational, but the aspiration used to somewhat resolve. You did the work, you got the life. Now you do the work and life keeps receding.

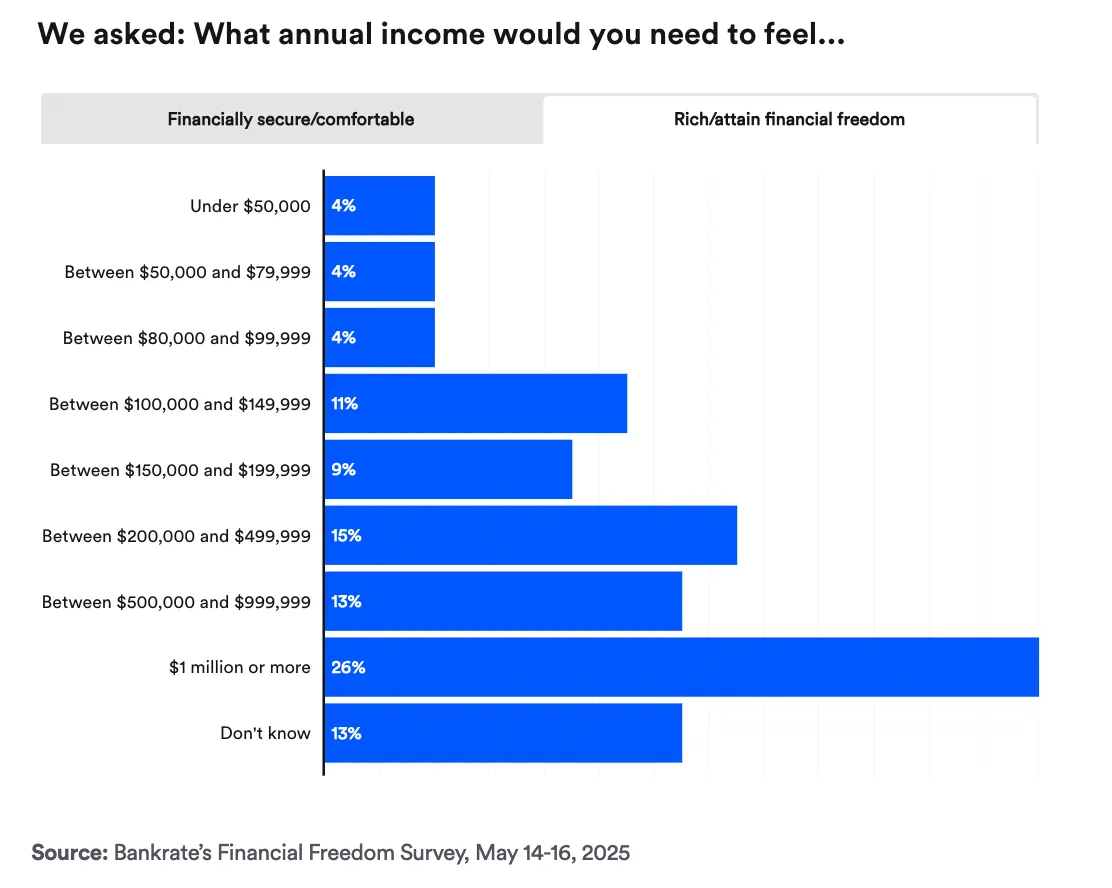

A Harris Poll for Fortune found that 64% of six-figure earners now describe their income as “survival mode, not wealth.” Goldman Sachs found that 41% of households earning $300K to $500K are living paycheck to paycheck. A majority of Americans say they’d need to earn $520,000 a year to feel rich.

The political scientist Peter Turchin has a framework for understanding this group historically. He calls it “elite overproduction”: Societies produce more people who expect elite positions than positions exist. It’s the engine of the American Dream running hotter than the economy can support. For example, master’s degrees have doubled since 2000. The credentials of elite status — the graduate degree, the knowledge-work title, the coastal zip code — have proliferated, while the economic substance has concentrated into a smaller and smaller group at the very top. You end up with an enormous class of people who did “everything right” and are one bad quarter away from the financial crisis.

Yes, many upper-middle-class households fall within the top 20% or even top 10% of earners. Statistically, they’re doing well. But the chasm between the upper middle class and the actual ownership class — the people whose wealth generates its own income without labor — is quite large, and widening. The top 20% accounts for 59% of all consumer spending. But within that top 20%, the real divide is between people who earn and people who own.

The line that actually matters

Which brings us to the thing both groups (material precarity and positional precarity) share: neither group is accumulating capital. And in an economy organized around returns to ownership, that’s the only thing that actually determines which side of the K you land on.

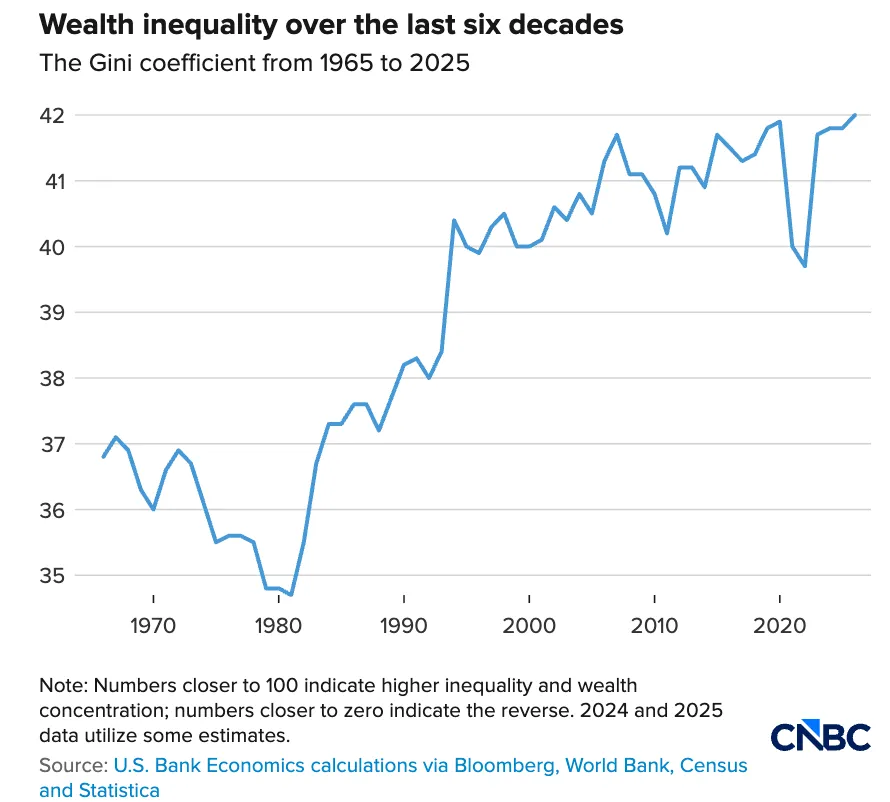

I’m going to simplify the structural economics here, because I’ve written about this in depth before, and the details are in those pieces. The short version: wealth in America is concentrating at the top at a rate that’s quickly accelerating. The top 1% (hell, 0.01%) owns the vast majority of stocks, real estate, and income-generating assets. Returns on capital historically outpace economic growth — meaning wealth grows faster if you already have it. And the tax code reinforces this.

So, if you’re on the labor side of the economy — earning a paycheck, no matter how large — you’re playing a different game than someone whose wealth generates its own returns. Money with Katie put it well: Once you’ve accumulated enough, the system gives you lower loan rates, higher deposit yields, and structural advantages that compound. Below that threshold, you’re earning income that gets taxed heavily, spending it on costs that inflate faster than wages, and trying to save the remainder into accounts that grow slower than the life you’re saving for.

The family earning $75K and the family earning $350K have more in common with each other — structurally, in terms of their relationship to capital — than either has with the family whose wealth generates its own income without labor. Both are running on the treadmill. One is running slower, but neither is able to get off.

What permanent instability does to your brain

This explains why both groups are exhibiting the same psychological response to our current economy, just at different price points: the inability to plan, to imagine a future, to trust that effort connects to outcomes.

Pew found that 41% of Americans now say the American Dream “was once possible but no longer.” Raj Chetty’s research shows that for people born in the 1980s, the probability of outearning your parents is basically a coin flip. That statistic alone reshapes how people relate to work, to saving, to the whole idea that the future is worth investing in.

And both groups — at very different income levels — are reaching for the same set of coping mechanisms. Kyla Scanlon calls it the progression from vibecession to “vibepression.” Fortune coined “disillusionomics” to describe how Gen Z is rejecting traditional financial paths entirely — turning to crypto, prediction markets, and content creation as income streams because the conventional ladder feels broken.

That’s how you get people who earn well but can’t bring themselves to open their bank accounts. People who know they should invest but keep the money in savings because the market “feels rigged.” People who doom spend and know it and can’t stop.

The financial behaviors are downstream of the psychological experience: When the future feels foreclosed, your brain starts optimizing for the present. And when you’ve internalized the idea that effort doesn’t connect to outcomes, you stop making the kinds of financial decisions that require believing in your own future.

The entire consumer economy depends on people wanting more — the next class, the next tier, the next milestone, the next upgrade. Some of the precarity both groups feel is structural (real costs, real wage stagnation, real policy failure). And some of it is our broader system working to keep you in a state of lack so you keep consuming, keep hustling, keep maxxing. Separating which part is structural and which part is manufactured dissatisfaction is one of the hardest psychological tasks there is.

Who gets blamed (and who doesn’t)

There’s a lot of economic resentment right now, and a lot of it gets misdirected in ways that serve the existing structure.

When you’re experiencing material precarity, the resentment tends to flow toward immigrants, toward the generation that came before you, toward the upper-middle-class “elites”. When you’re experiencing positional precarity, the resentment may flow toward people who “didn’t optimize hard enough,” toward the general sense that nobody appreciates how hard you’re working.

In both cases, the anger moves sideways or downward. It less often moves upward — toward the 0.1% whose effective tax rate is lower than yours, toward the policy choices that make wealth concentration a feature, not a bug. And it almost never turns into the question that actually matters: What would it take for me to move from the labor side of this economy to the ownership side?

Research on perceived mobility and populism shows that it’s the awareness of downward mobility — not the objective conditions — that drives radicalization. And the effect is strongest among people who feel they’re not meeting their parents’ standard of living. Sociologist Guy Standing’s work on the “precariat” maps this precisely: the fallen working class turns atavistic — nostalgic for a past economy that included them. The educated-but-blocked class turns progressive — demanding systemic reform. Both are responding to the same structural forces. But instead of recognizing that shared position, they organize against each other. The resentment becomes horizontal instead of vertical.

Meanwhile, instead of systemic solutions, the culture offers individual ones. Optimization culture. Side hustles. “Maxxing.” Career content that treats a structural problem like a personal productivity challenge. The treadmill gets faster, and instead of questioning the treadmill, we buy better shoes.

So what do you actually do with this

I’m not going to prescribe a policy solution. (I write a newsletter.) But as a financial planner and as someone who lives inside this exact tension, I think there are a few things worth sitting with:

- Name which precarity is yours. Money anxiety feels similar at every income level, but the mechanics are often different. If you’re in material precarity, the work is protecting the floor — building a buffer, reducing exposure to the extraction economy, making the system work for you where it can. If you’re in positional precarity, the work is harder to see because it’s quite psychological: separating what you need from what you were trained to expect.

- Understand the capital line. If you’re on the labor side of the economy — and most people reading likely are — the question isn’t “how do I earn more?” It’s “how do I convert labor income into ownership of appreciating assets?” Wages are taxed like income. Assets are taxed like wealth. The system rewards the second. Understanding this distinction is the beginning of agency, even if the path to acting on it looks different at every income level.

- Separate structural precarity from manufactured dissatisfaction. Some of what you feel is real — costs are up, the safety net is frayed, the economy is restructuring around capital. And some of what you feel is the consumer economy doing its job: keeping you in a state of aspirational lack so you keep spending, keep upgrading, keep chasing the next tier. Telling the difference between the two can help you actually build agency with your money.

And also — be suspicious of any analysis that makes you feel only helpless. The doom-scroll economy benefits from your nihilism. The people producing economic content online — including, yes, me — are disproportionately in the positionally precarious class, and our vantage point overrepresents a specific kind of existential dread. The internet is not the economy. Some of the doom is real. Some of it is a very specific class of writer describing their own anxiety and universalizing it. In other words, take everything with a grain of salt.

The dissonance you may be feeling right now — the gap between what the numbers say and what your life feels like — can be real. You’re likely perceiving a structural contradiction that the word “middle class” was designed to paper over.

But perception is also the beginning of agency. You can’t navigate what you can’t see. And now you can see it.

I should note that this system was built primarily for white men. The GI Bill was administered through local agencies that routinely discriminated against Black veterans. Redlining excluded Black families from the suburban wealth-building machine. The middle class was a policy project AND also, in many cases, racially exclusive one. ↩︎